Get Preapproved for a Mortgage Loan in New York’s: Living in New York, owning a home is a dream many have. Finding the perfect property and negotiating the deal is exciting. But getting mortgage preapproval can seem scary.

If you’re like me, mortgage financing can be overwhelming. But don’t worry, this guide will help you through it. By the end, you’ll know how to start your journey to homeownership in New York.

Key Takeaways

- Understand the difference between prequalification and preapproval for a mortgage loan in New York

- Discover the benefits of getting preapproved and how it can give you an edge in the competitive real estate market

- Learn about the essential requirements and documentation needed to secure a mortgage preapproval in New York

- Explore strategies to improve your credit score and maximize your chances of getting approved

- Discover the various down payment options and assistance programs available for first-time and low-income homebuyers in New York

Understanding Mortgage Preapproval in New York State

Getting into the mortgage world can feel overwhelming, especially for first-timers in New York. Knowing the difference between prequalification and preapproval helps a lot. Prequalification is a basic check of your finances. Preapproval, however, digs deeper into your credit and ability to buy a home.

Difference Between Prequalification and Preapproval

Prequalification is a quick, informal check that shows how much you might borrow. Preapproval, though, is a detailed review of your finances, including credit and income. It gives you a clear loan amount and interest rate, helping you negotiate better in New York.

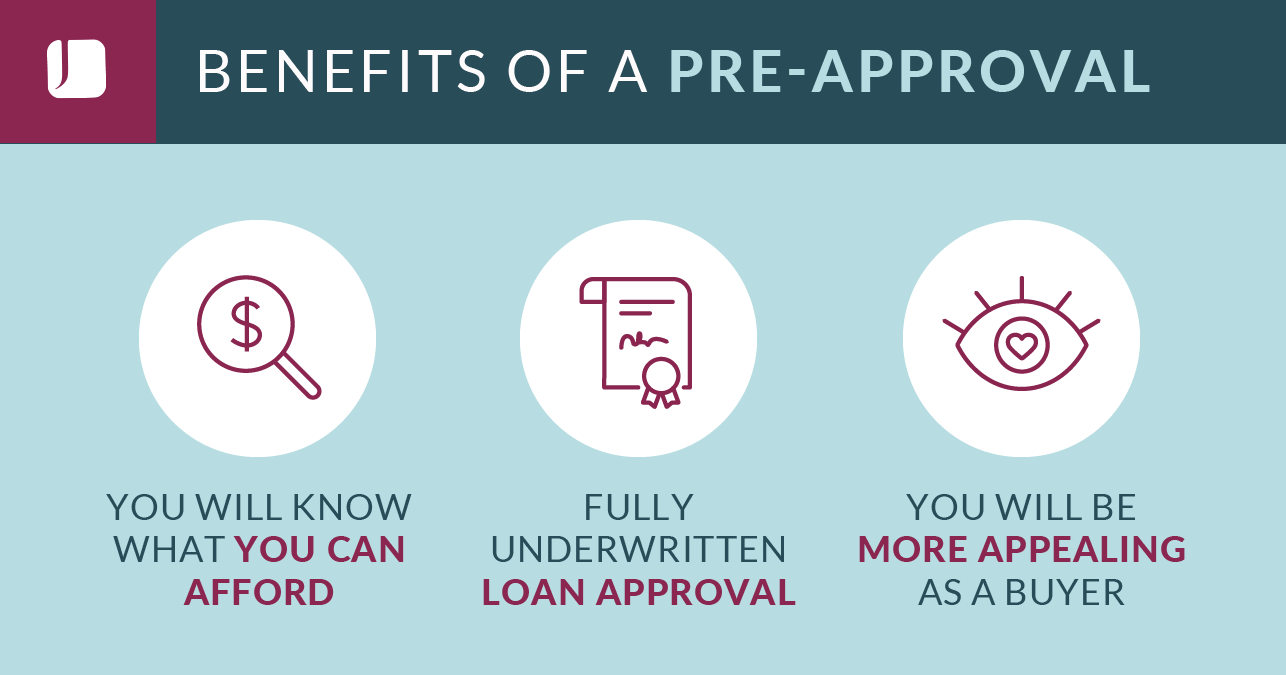

Benefits of Getting Preapproved

- Increased negotiating power when making offers on homes

- Faster closing process as you’ve already gone through the initial approval steps

- Ability to better budget and plan for your new home purchase

- Confidence in knowing your financing is in place

Timeline of the Preapproval Process

The preapproval process in New York usually takes 2-10 business days. This depends on the lender and your financial situation. The lender will check your credit, income, and job to see how much you can borrow and the interest rate.

| Step | Timeline |

|---|---|

| Application Submission | 1-2 business days |

| Document Verification | 3-5 business days |

| Underwriting Review | 2-3 business days |

| Preapproval Letter Issuance | 1 business day |

Understanding the preapproval process in New York is key to becoming a successful how to get preapproved for a mortgage loan in new york. It’s crucial for both first-time home buyers and experienced homeowners. This knowledge will help you find and secure your dream home.

Essential Requirements for New York Mortgage Preapproval

Getting a mortgage preapproval in New York means meeting several important criteria. As someone looking to buy a home, knowing the credit score, income checks, and debt limits is key. These are what lenders look at when they review your application.

Your credit score is very important. Lenders usually want a score of 620 or higher for regular loans. But, in places like New York, they might ask for even more. It’s a good idea to check your credit report and fix any mistakes before you apply for a mortgage.

Income checks are also a big part of the preapproval process. Lenders will look at your job history, pay stubs, and tax returns. They want to make sure you have enough money to pay for the mortgage every month.

Your debt-to-income (DTI) ratio is another important factor. Lenders like it when this ratio is 43% or less. This means your monthly debt payments, including the mortgage, shouldn’t be more than 43% of your monthly income. A low DTI ratio shows you can handle the mortgage payments.

| Requirement | Typical Threshold |

|---|---|

| Credit Score | Minimum 620 for conventional loans |

| Income Verification | Stable employment history, pay stubs, tax returns |

| Debt-to-Income (DTI) Ratio | Preferred 43% or less |

Knowing these key requirements for mortgage preapproval in New York helps you get ready. It increases your chances of getting the loan you need to buy a home.

Credit Score Requirements and Impact on Your Application

As a first-time homebuyer in New York, your credit score is key to getting a mortgage. Knowing the minimum score needed and how to boost it can greatly help you on your path to owning a home.

Minimum Credit Score Requirements

The credit score needed for a mortgage varies by loan type. Conventional loans usually need a score of at least 620. But, government-backed loans like FHA and VA might accept lower scores. Still, a higher score can mean better interest rates and loan terms.

How to Improve Your Credit Score

- Pay all your bills on time to build a positive payment history.

- Keep your credit card balances low, ideally below 30% of your credit limit.

- Regularly review your credit report for any errors or inaccuracies and dispute them with the credit bureaus.

- Avoid opening new credit accounts unless necessary, as this can temporarily lower your credit score.

Impact of Credit History on Interest Rates

Your credit history affects not just your mortgage eligibility but also the interest rate you get. Those with higher scores often get lower rates. This means lower monthly payments and big savings over time. For first-time homebuyers in New York, this is especially crucial due to the high cost of living.

“Improving your credit score can save you thousands of dollars over the life of your mortgage.”

Income Verification and Employment History Documentation

When you apply for a mortgage loan in New York, lenders check your income and job history. They want to see if you can afford monthly payments. You’ll need to give them documents to prove your income and job stability.

To show your income, you’ll need to collect the following documents required for mortgage preapproval:

- Recent pay stubs covering a 30-day period

- W-2 forms from the last two years

- Federal tax returns from the past two years

- Proof of any additional income, such as rental properties, investments, or bonuses

Also, new york home buyers must show their job history. This includes:

- Letter of employment from your current employer, confirming your position, income, and length of service

- Recent pay stubs or bank statements showing consistent income deposits

- If self-employed, a profit and loss statement, balance sheet, and two years of tax returns

Lenders look at this info to check if you’re financially stable. They want to make sure you can pay your mortgage. By getting these documents required for mortgage preapproval ready early, you make the new york home buyers preapproval process smoother. It shows you’re ready for lenders.

| Document | Purpose |

|---|---|

| Pay stubs | Verify current income |

| W-2 forms | Confirm past two years of income |

| Tax returns | Validate income from all sources |

| Employment letter | Prove job stability and position |

| Bank statements | Demonstrate consistent income deposits |

“Thorough documentation is key to securing mortgage preapproval in New York. Be prepared to provide a comprehensive financial snapshot to lenders.”

How to Get Preapproved for a Mortgage Loan in New Yorks

Getting preapproved for a mortgage in New York is easy with the right help. It doesn’t matter if you’re buying your first home or investing. Knowing the steps, what documents you need, and what to avoid can help you get a mortgage preapproval. This gives you an edge in the real estate market.

Step-by-Step Application Process

The first thing to do is gather your financial info and documents. You’ll need your income, job history, credit score, and any debts. With this ready, you can start applying with a lender.

- Give your personal and financial details to the lender.

- Let the lender check your credit report to see if you qualify.

- Send in your documents, like pay stubs, tax returns, and bank statements.

- Wait for the lender to review your application and give you a preapproval letter for mortgage.

Required Documentation Checklist

- Proof of income (pay stubs, W-2 forms, tax returns)

- Bank statements (checking, savings, and investment accounts)

- Photo ID (driver’s license or passport)

- Social Security number

- Details about any debts you have (credit cards, auto loans, student loans)

Common Application Mistakes to Avoid

To make the mortgage preapproval process smooth, avoid common mistakes. Some mistakes include:

- Not giving accurate and current financial info

- Ignoring credit issues or bad marks on your report

- Not keeping your job and income stable

- Applying for new credit or big purchases during the process

By following these steps and avoiding these mistakes, you can boost your chances of getting a mortgage preapproval in New York. This is a big step towards owning your home.

Understanding Debt-to-Income Ratio Requirements

When you apply for a mortgage in New York, lenders check your debt-to-income (DTI) ratio closely. This key factor helps decide if you qualify and how much you can borrow. Knowing how to figure out and boost your DTI is key for a smooth mortgage preapproval.

Your debt-to-income ratio shows what part of your monthly income goes to debt payments. This includes credit cards, car loans, student loans, and other regular debts. Lenders usually want a DTI of 43% or less. This shows you can handle your finances and make mortgage payments on time.

- To find your DTI ratio, add up your monthly debt payments and divide by your monthly income.

- For instance, if your monthly debt is $2,000 and your income is $5,000, your DTI is 40% ($2,000 / $5,000 = 0.40).

Boosting your debt-to-income ratio can help you get mortgage preapproval in New York. Here are some ways to do it:

- Pay down existing debts to reduce your monthly payments.

- Boost your income with a new job, promotion, or side hustle.

- Don’t take on new debt before applying for a mortgage.

By understanding the debt-to-income ratio needs and working to improve your finances, you can confidently go through the new york mortgage process. This can help you get the best mortgage terms possible.

Down Payment Options and Assistance Programs

Buying a home in New York is a big deal. The down payment can be a big challenge for first-time buyers. But, there are many down payment assistance programs and options to help.

First-Time Homebuyer Programs

If you’re a first-time homebuyer in New York, you might qualify for special help. These programs offer financial aid or lower down payment needs. They can help make your dream of owning a home come true.

New York State Grant Programs

New York has several grant programs for down payment assistance. These grants target certain groups, like first-time buyers or those with lower incomes. They aim to make owning a home more possible.

FHA Loan Requirements

The FHA loan is a great choice for first-time homebuyers in New York. It requires a down payment as low as 3.5% of the home’s price. This makes it easier for those with less savings to get into the market.

Exploring these down payment assistance options can help you start your journey to homeownership in New York. With the right help and information, owning a home becomes more within reach.

Choosing the Right Mortgage Lender in New York

Looking to buy a home in New York? Picking the right mortgage lender is key. With many lenders around, it’s important to find one that fits your financial needs. Here are some things to think about when choosing a mortgage lender in New York:

Interest Rates and Fees

It’s vital to compare interest rates and fees. Mortgage lenders in New York offer different rates and programs. Look for the best deals by comparing APR, origination fees, and other loan costs.

Customer Service and Reputation

Good customer service can make a big difference. Talk to new york home buyers and read reviews online. A lender known for great service can make your experience smoother.

Specialized Programs and Expertise

Some lenders in New York focus on specific needs, like first-time buyers. Look for lenders with programs that match your situation. This can lead to better terms and a better experience.

By considering these factors, you can make a smart choice. The right lender can greatly improve your home-buying journey. Remember, a well-thought-out choice can make a big difference.

“Working with the right mortgage lender can make all the difference in the world when it comes to securing a home in New York.”

What Happens After Preapproval

Getting a preapproval letter for your mortgage in New York is a big step in buying a home. But what’s next? Knowing how long your preapproval is good for and what comes next in the mortgage process can make things easier.

Validity Period of Preapproval Letter

A preapproval letter usually lasts from 60 to 90 days. This means you can look for homes, knowing you’ve been approved for a certain amount. But remember, this approval isn’t a final yes. Your lender might check your info again if it takes longer to buy a home.

Next Steps in Home Buying Process

- Start house hunting: With your preapproval, you can look for homes in New York. Work with a real estate agent to find homes that fit your budget and what you like.

- Make an offer: When you find the right home, your agent will help you make a strong offer. You’ll negotiate the price and other details with the seller.

- Secure a home inspection: Before buying, get a detailed home inspection. This checks if the home is in good shape and finds any problems.

- Complete the mortgage process: Your lender will help you finish the mortgage steps. This includes finalizing your loan application, getting appraisals, and closing on the home.

The preapproval is just the start of buying a home in New York. By knowing what comes next and working with your lender and agent, you can make the transition to your new home smooth and successful.

| Step | Description |

|---|---|

| Preapproval | Lender reviews your financial information and approves you for a loan amount. |

| House Hunting | Shop for a home with your preapproval letter, knowing your budget and loan eligibility. |

| Offer and Negotiation | Work with your agent to submit a competitive offer and negotiate the purchase price. |

| Home Inspection | Arrange for a comprehensive inspection to ensure the property is in good condition. |

| Mortgage Finalization | Complete the remaining steps in the mortgage process, including appraisals and closing. |

Comparing Different Types of Mortgage Loans

When looking for a mortgage in New York, you have many options. Knowing the good and bad of each can help you choose wisely. This is especially true for mortgage lenders in new york and first-time homebuyers in new york.

Conventional Mortgages

Conventional mortgages are a favorite choice. They often need a down payment of at least 20% of the home’s value. These loans have good interest rates and are best for those with strong credit and steady income.

FHA Loans

Federal Housing Administration (FHA) loans are great for first-time buyers or those with lower credit. You only need a 3.5% down payment. They also have more flexible credit rules, making them easier to get.

VA Loans

VA loans are for military members, veterans, and their spouses. They offer 100% financing, no down payment, and low interest rates. This makes them a great choice for those who qualify.

USDA Loans

United States Department of Agriculture (USDA) loans help low-income and moderate-income people in rural areas. They have no down payment and lower interest rates. They’re a good option if you meet the income and location requirements.

| Loan Type | Down Payment | Credit Score Requirements | Eligibility |

|---|---|---|---|

| Conventional | 20% or more | Minimum 620 | Borrowers with strong credit and income |

| FHA | 3.5% | Minimum 580 | First-time homebuyers, low-income borrowers |

| VA | 0% | Minimum 580 | Active military, veterans, and their spouses |

| USDA | 0% | Minimum 640 | Low-income borrowers in eligible rural areas |

Understanding each mortgage loan’s unique features and requirements helps. This way, mortgage lenders in new york and first-time homebuyers in new york can make a choice that fits their financial goals and personal situation.

Conclusion

Starting your journey to homeownership in New York? Getting preapproved for a mortgage loan is key. Understanding the process, meeting requirements, and choosing good lenders will help you. You’ll be closer to owning a home in the Empire State.

Success in mortgage preapproval in New York starts with preparation. Check your credit score, collect needed documents, and figure out your debt-to-income ratio. This way, you’ll feel confident and ready to apply for your loan.

With the right strategy and help from experienced lenders, you can explore many options in New York’s real estate market. This article gives you the knowledge and tools to move forward. Whether you’re buying your first home or investing, you’re ready to start your journey. Begin your path to homeownership in New York today.

FAQ

What is the difference between mortgage prequalification and preapproval?

Prequalification is an early check of how much you can borrow. It’s based on what you tell the lender about your finances. Preapproval, on the other hand, is a deeper look at your credit, income, and assets. It gives you a conditional approval for a specific loan amount.

What are the benefits of getting preapproved for a mortgage in New York?

Getting preapproved makes you a more appealing buyer. It helps you know your budget. Plus, it might get you better interest rates and loan terms than not being preapproved.

How long does the mortgage preapproval process typically take in New York?

The time it takes for preapproval varies. It can be a few days to a few weeks. Giving all needed documents early can speed things up.

What are the minimum credit score requirements for mortgage preapproval in New York?

The credit score needed varies by loan type. But, most lenders in New York want a score of at least 620 for conventional loans. FHA loans might accept scores as low as 580.

How can I improve my credit score to get better mortgage rates in New York?

To boost your credit score, pay down debt and fix any credit report errors. Keep your payments on time. Also, watch your credit utilization ratio and avoid new credit applications before applying for a mortgage.

What types of income and employment documentation are required for mortgage preapproval in New York?

Lenders need recent pay stubs, W-2 forms, tax returns, and proof of extra income. They might also ask for job history documents like letters from your employer or proof of a stable job.

What is the step-by-step process for getting preapproved for a mortgage in New York?

First, gather all needed documents. Then, apply for preapproval with a lender. Next, you’ll go through a credit check and financial review. After that, you’ll get a preapproval letter. Finally, use this letter when making offers on homes.

How do lenders calculate the debt-to-income ratio for mortgage preapproval in New York?

Lenders calculate your debt-to-income ratio by dividing your total monthly debt by your monthly income. Most prefer a ratio under 43%. But, some may accept higher ratios based on your financial situation and the loan program.

What down payment assistance programs are available for first-time home buyers in New York?

New York has several programs for first-time buyers. The New York State Homes and Community Renewal (HCR) program and city-specific initiatives offer grants, low-interest loans, or other help for down payments and closing costs.

How do I choose the right mortgage lender in New York?

Look at interest rates, loan fees, customer service, and experience with first-time buyers. Compare offers from different lenders to find the best deal.

What happens after I receive my mortgage preapproval letter in New York?

Your preapproval letter is good for 60-90 days. Use it to find and make offers on homes. Once you have an offer accepted, you’ll need to apply fully and provide more documents to the lender.