10 Factors That Impact Your Home Insurance Rate: Getting the right insurance for your home is crucial. But, did you know many things can change how much you pay for home insurance? In this article, we’ll look at the top 10 things that affect your home insurance rates. We’ll also share tips to help you save money.

Key Takeaways

- Home insurance rates are influenced by a variety of factors, including property value, location, and safety features.

- Understanding how insurance companies assess risk can help you make informed decisions about your coverage.

- Regular maintenance and upgrades to your home can potentially lower your insurance premiums.

- Bundling your home insurance with other policies, such as auto insurance, can lead to significant savings.

- Maintaining a good credit score and claims history can also contribute to more favorable insurance rates.

Understanding Home Insurance Rate Basics

Home insurance premiums are more than just a number. Insurance companies look at risk factors to set your rates. Knowing how they work can help you understand homeowners insurance costs and factors affecting home insurance.

How Insurance Companies Calculate Your Premium

Insurance providers have a detailed method to figure out your premium. They look at your home’s value, construction, and location. They aim to match the risk with a fair rate for claims.

The Role of Risk Assessment in Rate Determination

The core of premium calculation is risk assessment. They check crime rates, fire station proximity, and natural disaster risks. These risk factors affect your homeowners insurance costs to cover claims.

Knowing how insurance companies calculate your premium and the role of risk assessment is key. It helps you protect your home better.

Property Value and Construction Type

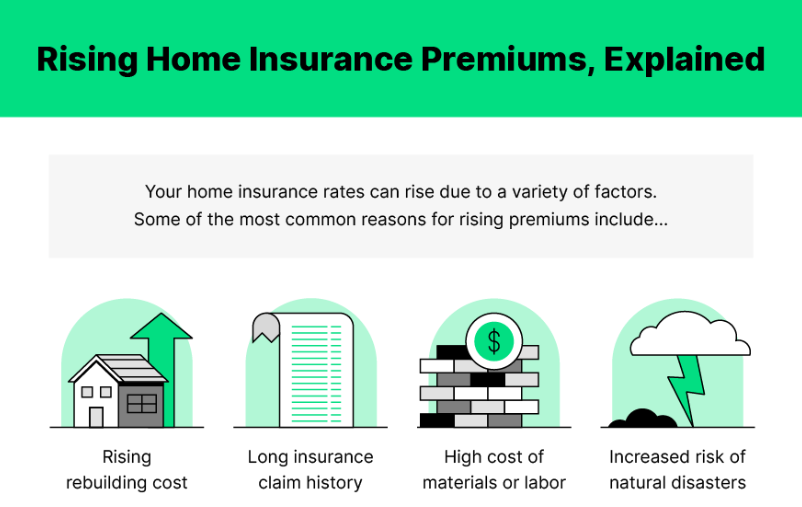

Home insurance rates depend on your property’s value and construction. Insurers look at the rebuild cost of your home to set your premium. Homes with higher rebuild costs usually have higher insurance rates.

The materials used in your home’s construction also matter. Homes with fire-resistant materials like brick or steel often have lower insurance rates. The age and condition of your home’s systems, like the roof and plumbing, also affect your rates.

To get the right coverage and rates, it’s key to have your home assessed. You can work with a professional appraiser or use online tools to estimate your home’s value. Knowing how your property’s features affect your insurance can help you save money.

| Home Construction Type | Estimated Impact on Insurance Rates |

|---|---|

| Brick or Concrete | Lower rates |

| Wood Frame | Higher rates |

| Metal or Steel | Lower rates |

| Older Home (over 20 years) | Higher rates |

Understanding how your property value and construction type affect your home insurance rates helps you make smart choices. This way, you can keep your insurance costs under control.

Location and Environmental Risk Factors

Your home’s location greatly affects your insurance costs. Things like neighborhood crime rates, natural disaster risks, and how close you are to fire stations matter. These factors can change how much you pay for insurance.

Neighborhood Crime Statistics Impact

Insurance companies watch crime rates in your area. Places with more break-ins and vandalism are seen as riskier. This can make your home insurance premiums go up.

Getting a good home security system can help lower your rates. It shows you’re serious about keeping your home safe.

Natural Disaster Prone Areas

If your home is near natural disasters like hurricanes or floods, you’ll pay more for insurance. Companies look at the chance of claims in these areas. Knowing your area’s risk helps you manage your home insurance costs.

Distance from Fire Stations and Hydrants

How close your home is to fire stations and hydrants also matters. Being far from these can mean more damage in a fire. This can lead to higher insurance rates.

Being close to these emergency services can help lower your costs. It shows your home is easier to reach in an emergency.

Understanding how your location affects your home insurance can help you save money. You can make choices that lower your monthly costs.

Claims History and Insurance Score

Your claims history and insurance score are key in setting your home insurance rates. Insurers look at your past claims and credit to see how risky you are. Knowing how these affect your rates helps you save on insurance costs.

Your claims history shows if you’re likely to file more claims. If you’ve filed many claims, insurers might see you as riskier. This can lead to higher insurance premiums. Keeping your claims record clean by avoiding unnecessary claims can help you get lower insurance premiums.

Your insurance score, based on your credit history, is also important. Insurers use this score to judge your financial responsibility. Improving your credit score can lower your home insurance rates. Paying bills on time, reducing debt, and checking your credit report for errors can help improve your score.

| Factors Affecting Claims History | Strategies to Improve Insurance Score |

|---|---|

| Number of past claims Claim amounts Claim frequency Type of claims (e.g., theft, natural disasters) | Pay bills on time Reduce outstanding debt Check for errors in credit report Maintain a healthy credit mix |

Understanding how claims history and insurance score affect your managing home insurance premiums lets you take steps to lower your rates. This way, you can get more affordable home coverage.

“A clean claims history and a strong insurance score can significantly lower your home insurance premiums, saving you money in the long run.”

Home Security and Safety Features

Home safety features can help lower your home insurance rates. Insurance companies give discounts for homes with safety measures. These measures reduce the risk of claims.

Security System Benefits

Getting a professional security system can save you money on insurance. These systems scare off burglars and alert authorities fast. This means less damage and lower insurance costs.

Impact of Safety Installations

- Smoke detectors and fire extinguishers cut down fire claim risks. This can save you on insurance.

- Storm shutters and strong windows protect against weather damage. This makes your home more appealing to insurers.

- Deadbolt locks and security lights make your home safer. This lowers the chance of break-ins and claims.

Smart Home Technology Advantages

Smart home tech offers new ways to save on insurance. Features like remote security systems and water detectors show your home is well-protected. This can lead to more discounts.

| Safety Feature | Potential Discount |

|---|---|

| Burglar alarm system | 5-20% |

| Smoke detectors | 2-5% |

| Fire extinguishers | 1-3% |

| Storm shutters | 5-15% |

| Smart home technology | 5-10% |

Investing in home safety can protect your property and lower insurance rates. Talk to your insurance provider about discounts and how to save more.

10 Factors That Impact Your Home Insurance Rate and How to Control Them

Understanding home insurance can be tough. But knowing what affects your rates is key to saving money. This guide will cover the 10 main factors that influence your rates. We’ll also give tips on how to manage them.

- Property Value and Construction Type – Make sure your home’s value is right. Look into affordable upgrades to materials that might lower your premiums.

- Location and Environmental Risk Factors – Check your area’s crime rates and how close you are to fire stations. Also, take steps to lessen natural disaster risks.

- Claims History and Insurance Score – Keep your claims record clean. Also, watch your insurance score to show you’re a reliable policyholder.

- Home Security and Safety Features – Get a security system and smoke alarms. These can lower your risk and get you discounts.

- Credit Score and Financial History – Know how your credit score impacts your rates. Work on improving it to save money.

- Coverage Limits and Deductible Choices – Find the right balance between coverage and cost. This affects your premiums.

- Home Age and Maintenance Status – Keep your home in good shape. Upgrading older systems shows you’re a responsible owner.

- Policy Bundling and Available Discounts – Look for chances to bundle policies or get discounts. This can save you money.

By tackling these 10 factors, you can control your home insurance rates. This ensures you get the best value for your money. A bit of research and planning can help manage your costs.

Knowing what affects your home insurance rates and managing them can save you a lot. Focus on these 10 factors to optimize your coverage. This protects your most valuable asset.

Credit Score and Financial History

Your credit score is key in setting your home insurance rates. Insurance companies look at your credit score to see how risky you are. Knowing this can help you boost your credit and lower your insurance premiums.

Understanding Credit-Based Insurance Scores

Credit-based insurance scores come from your credit report. They look at how you’ve paid bills, used credit, and how long you’ve had credit. Insurers think people with bad credit might file more claims.

Improving Your Credit for Better Rates

To get a better credit score and lower homeowners insurance rates, try these tips:

- Always pay your bills on time. This is the biggest part of your credit score.

- Don’t let your credit card balances get too high. Try to use less than 30% of your limit.

- Don’t apply for too many new credits. Each one can lower your score a bit.

- Check your credit report often for mistakes and fix them with the credit bureaus.

- Keep old credit accounts open. This shows you’ve had credit for a long time.

Improving your credit score can lead to lower insurance premiums and reduce homeowners insurance costs. Keep an eye on your credit and fix any problems to save money over time.

Coverage Limits and Deductible Choices

Choosing the right coverage limits and deductibles is key to managing your home insurance premiums. It’s important to find a balance between enough protection and keeping costs down.

Your coverage limits show the max your insurance will pay for a claim. Higher limits mean higher home insurance premiums. But, make sure your limits cover your home and belongings well.

Your deductible is what you pay before your insurance helps. A higher deductible lowers home insurance premiums. But, you’ll pay more when you file a claim.

Think about your money and how much risk you can handle. A higher deductible might be okay if you have savings. But, a lower deductible could be better if you want less financial stress.

| Coverage Limit | Deductible | Impact on Premiums |

|---|---|---|

| Higher | Lower | Increased premiums |

| Lower | Higher | Decreased premiums |

Knowing how coverage limits, deductibles, and home insurance premiums work together helps you make smart choices. You can keep costs down while still protecting your home and finances.

Home Age and Maintenance Status

The age and upkeep of your home greatly affect home insurance rates. Insurers see older homes and those not well-maintained as higher risks. But, homes in good shape, old or new, might get lower home insurance rates.

Impact of Regular Maintenance

Keeping your home’s big systems in check can lower home insurance rates. Fixing issues like roofing, plumbing, electrical, and HVAC early shows you’re managing risks. This effort often leads to better home insurance rates.

Major Systems and Their Condition

- Roof: A good roof can lower home insurance rates by preventing leaks and damage from the weather.

- Plumbing: A well-kept plumbing system can avoid expensive water damage claims, helping to lower home insurance rates.

- Electrical: Keeping your electrical system updated and maintained can reduce fire hazards, leading to lower home insurance rates.

- HVAC: Regular HVAC service can lower home insurance rates by reducing the chance of equipment failures.

By focusing on regular maintenance and fixing issues with your home’s major systems, you show insurers you’re serious about lowering home insurance rates. This proactive approach to risk management can pay off.

Policy Bundling and Available Discounts

As a homeowner, you can lower your insurance costs. This is by using policy bundling and discounts. Bundling your home insurance with auto or life insurance can save you a lot.

Insurance companies give discounts for bundling policies. This makes managing your insurance easier and can lower your insurance premiums. By combining policies, you might get bundling discounts that cut down your homeowners insurance costs.

There are also other discounts to look for to lower your homeowners insurance costs. These include discounts for:

- Installing a home security system

- Implementing fire and safety features

- Maintaining a claims-free history

- Owning an older, well-maintained home

- Belonging to certain professional or alumni associations

Understanding the bundling discounts and other discounts can help you save. It lets you create a plan to reduce homeowners insurance costs and get the best coverage.

| Discount Type | Average Savings |

|---|---|

| Bundle Discount | 5-25% |

| Home Security System | 2-15% |

| Claim-Free History | 5-20% |

| Mature Homeowner | 3-10% |

| Professional/Alumni Association | 2-10% |

Using bundling discounts and looking for other discounts can help you save. It’s a way to make sure you’re getting the best deal for your insurance.

Conclusion

Your home insurance rate is influenced by many factors. These include the value and construction of your property, your claims history, and your home’s security features. By understanding these, you can improve your home insurance coverage and possibly lower your premiums.

There are many ways to control your home insurance costs. You can make your home safer, keep it well-maintained, or look into bundling and discounts. Regularly checking your policy and making smart choices can help you get the right protection at a good price.

Your home is a valuable asset, and the right insurance is crucial. By staying informed and adjusting to changes in your insurance rates, you can find a balance. This balance ensures you have the protection you need without breaking the bank.

FAQ

What are the key factors that impact my home insurance rate?

Several things can change your home insurance rate. These include your home’s value, where it’s located, and any claims you’ve made. Also, safety features, risks from natural disasters, your credit score, and your policy details matter.

How can I control my home insurance premiums?

To manage your home insurance costs, know what risks your home faces. Improve your home and keep a clean claims record. A better credit score and smart policy choices can also help. Don’t forget to look for discounts and bundle policies for savings.

How does the location of my home affect my insurance rates?

Where your home is located greatly affects your insurance rates. Crime rates, fire station proximity, and natural disaster risks all play a part. These factors determine your risk level and premium costs.

What kind of home security and safety features can help lower my insurance rates?

Adding security systems, smoke detectors, and fire extinguishers can get you discounts. Smart home tech that boosts security can also save you money on premiums.

How does my credit score affect my home insurance rates?

Insurance companies use your credit score to judge risk. A good score can lead to lower rates. So, keeping your credit in check is key to saving on insurance.

How do my coverage limits and deductible choices impact my insurance premiums?

Your policy’s coverage limits and deductibles greatly influence your premiums. Higher deductibles and lower limits can cut costs. But, choose wisely to meet your financial and risk needs.

Can bundling my home and auto insurance policies save me money?

Yes, bundling home and auto policies with one provider can save you up to 25% or more. It’s a smart way to reduce your insurance costs with the discounts many companies offer.